Your credit score plays a major role in your financial life. From qualifying for loans to determining interest rates, understanding your credit score can help you make smarter financial decisions and boost your score over time. In this guide, we’ll cover what credit score do you start with, ways to build credit, and answer common questions like what credit score is needed to buy a car.

What Is a Credit Score?

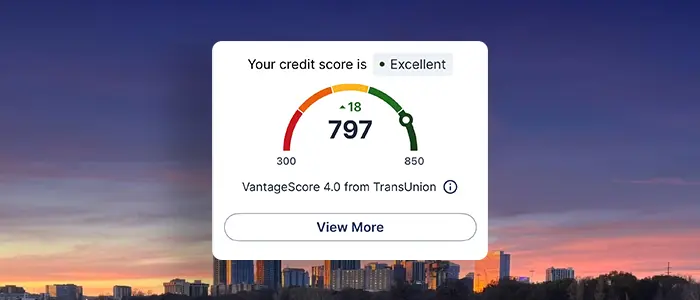

A credit score is a numerical representation of your credit risk at a particular point in time. Scores typically range from 300 to 850, depending on the scoring model. The higher your score, the better your credit profile. Credit scores change as you add, update, or remove information from your credit report.

Many people wonder, “what is the most accurate credit score?” While no single score is perfect, FICO® and VantageScore® are widely recognized as reliable scoring models used by most lenders.

What Credit Score Do You Start With?

If you are new to credit, you may wonder what credit score do you start with. Most new borrowers start with no score, as scoring models require a credit history to calculate a number. Once you open your first credit account, your activities — such as making on-time payments and keeping balances low — begin to build your score.

How Credit Scores Are Calculated

Credit scores are calculated using information in your credit report. The major credit reporting agencies are Equifax, Experian, and TransUnion. They collect data from lenders to track your credit habits. Scores are generated using complex algorithms that predict your likelihood of repaying debts.

Main Factors That Affect Your Credit Score:

- Payment history (35%) – Always pay on time. This is the most important factor.

- Amounts owed (30%) – Keep balances low on revolving credit like credit cards.

- Length of credit history (15%) – The longer your accounts are open, the better.

- New credit (10%) – Opening multiple accounts at once can lower your score temporarily.

- Types of credit in use (10%) – A healthy mix of credit types can be beneficial.

Ways to Build Credit and Improve Your Score

Knowing how to build credit is key to boosting your financial opportunities. Here are proven ways to build credit:

- Pay bills on time – Late payments, collections, and bankruptcies hurt your score. Knowing when to pay your credit card bill to increase credit score can help. Pay before the due date, always try and pay the statement balance in full, and keep use low.

- Keep balances low – High balances relative to credit limits can negatively impact your score.

- Open new credit accounts only as needed – Don’t open accounts just to improve your credit mix.

- Pay off debt instead of moving it – Avoid using short-term strategies like closing cards to boost your score.

- Check your credit report for errors – Correct any mistakes to ensure your score is accurate.

Read Six Tips for Improving Your Credit Score for more ways to improve credit.

Frequently Asked Questions About Credit Scores

Q: What is the lowest credit score possible?

A: The lowest credit score depends on the scoring model, but most range from 300 (the lowest credit score possible) to 850.

Q: What do the credit reporting agencies call their FICO score?

A: The major agencies have their own names for the score:

- Equifax: BEACON

- Trans Union: EMPIRICA

- Experian: Experian/Fair Isaac Risk Model

Q: Why do lenders use credit scores?

A: Credit scores give a fast and objective measurement of credit risk. Credit risk refers to the risk to the lender that the borrower will not repay the loan as agreed. Borrowers who make late payments or don't repay everything they owe are an expensive problem for all lending institutions. The extra costs and losses involved make borrowing more expensive for everyone.

Q: What’s a good credit score to buy a car?

A: Lenders may approve car loans with scores as low as 580–600, but higher scores will get you better rates.

Q: Why are there different credit scores?

A: You may see different credit scores depending on the scoring model (FICO® vs. VantageScore®), the bureau providing the information (Experian, Equifax, or TransUnion), and the timing of lender reports. Each bureau may have slightly different data, so it’s normal for your scores to vary.

Q: How can Credit Coach1 in Digital Banking help me?

A: Credit Coach gives real-time access to your credit score, personalized tips to improve it, and alerts when changes occur. It’s an easy way to monitor your credit, spot errors, and boost your score over time.

1 Members must be 18 years of age or older with a valid Social Security Number. Credit monitoring services are provided through our partnership with Credit Coach.

See Terms and Conditions for Online Banking.